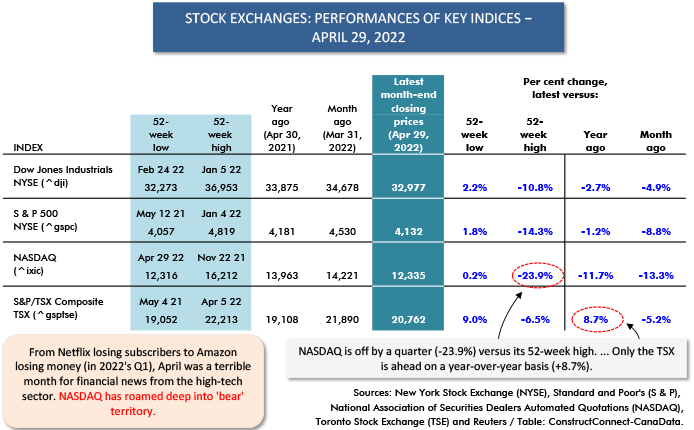

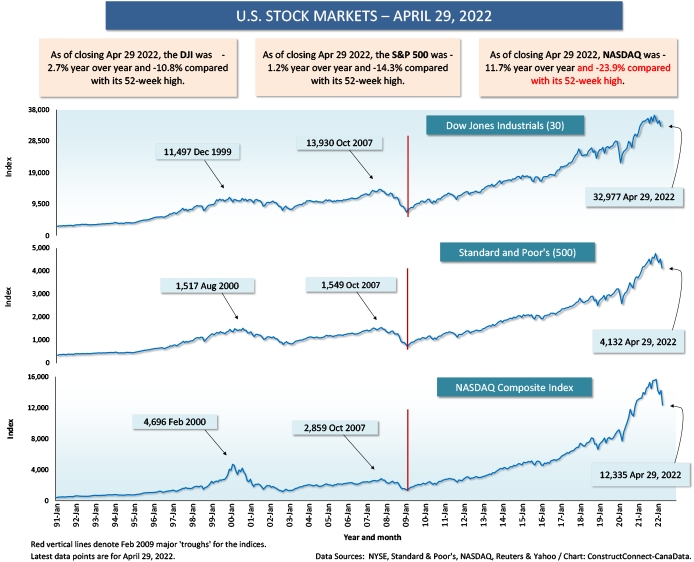

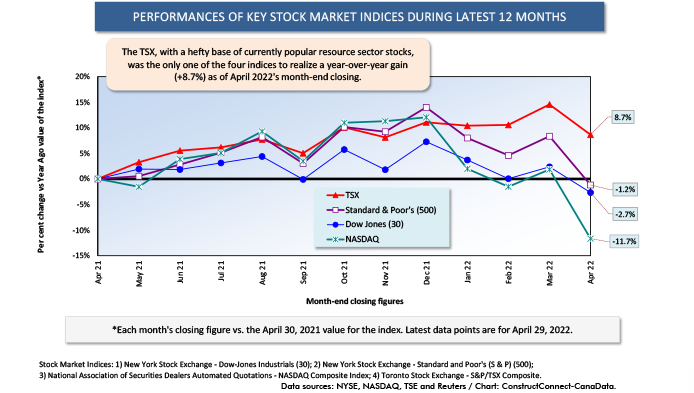

April was not a good period for stock markets. In North America, on a month-to-month basis, the DJI was -4.9%; the TSE -5.2%; the S&P 500, -8.8%; and NASDAQ, -13.3%.

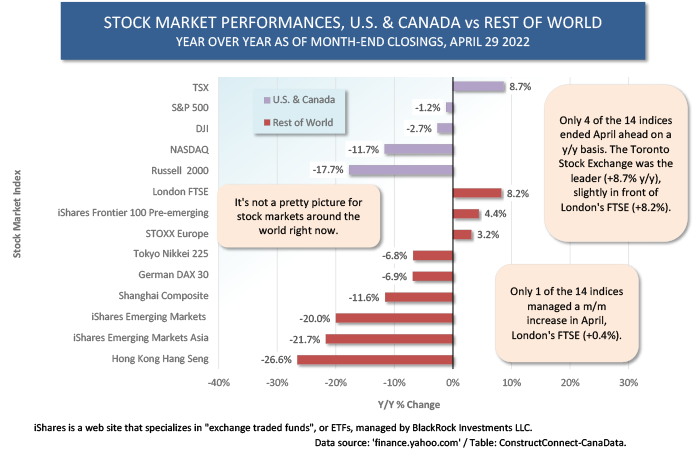

On a year-over-year basis, only the Toronto Stock Exchange (TSE), which has a heavy weighting of resource sector firms, managed a gain, +8.7%. (Commodity prices have been on an upswing.) The S&P 500 was -1.2% y/y; the DJI, -2.7%; and NASDAQ, -11.7%.

On a year-over-year basis, only the Toronto Stock Exchange (TSE), which has a heavy weighting of resource sector firms, managed a gain, +8.7%. (Commodity prices have been on an upswing.) The S&P 500 was -1.2% y/y; the DJI, -2.7%; and NASDAQ, -11.7%.

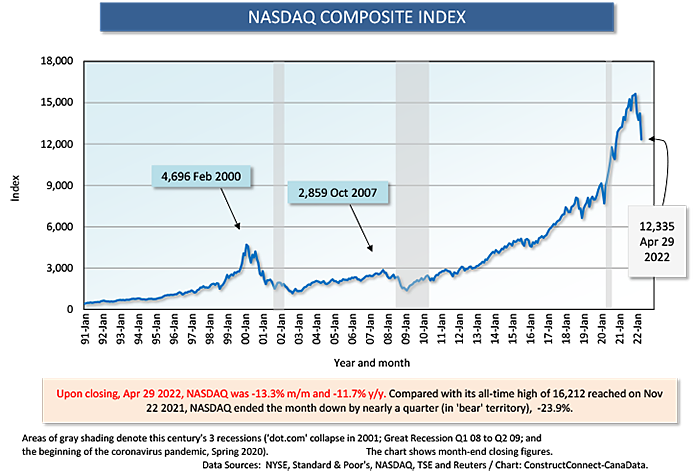

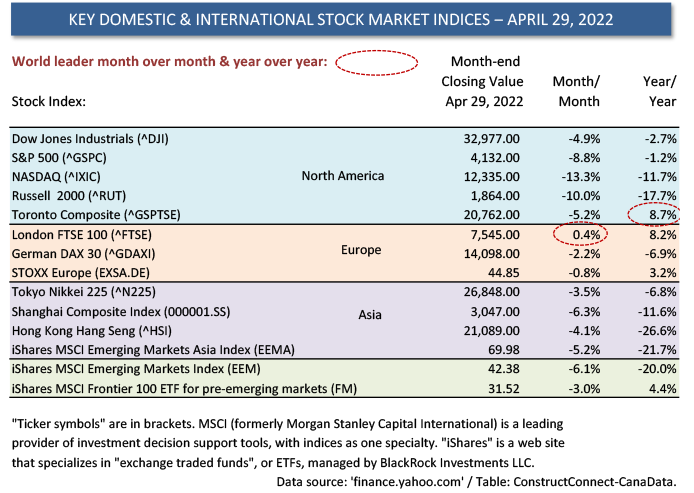

Versus its 52-week high, NASDAQ was a stunning loser, at -23.9%. A drop of -20.0% or worse is known as ‘bear’ territory. The Russell 2000 index, for small cap firms, was also bearish in April, at -24.2% compared with its peak.

Several of the biggest high-tech firms have been missing profit targets (Meta), or suffering unexpected and uncharacteristic losses (Amazon), or seeing reductions in their number of subscribers (Netflix).

Runaway inflation and its unwelcome companion, interest rate hikes, have also been suppressing the investment sentiment of day traders, hedge funds and brokerage houses.

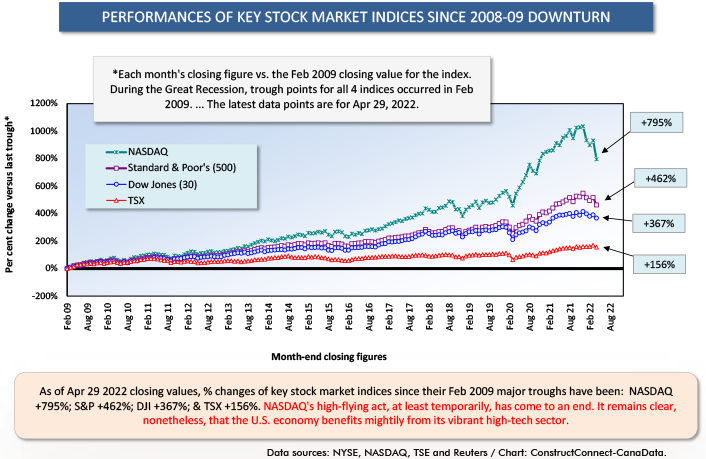

The net effect has been a pummeling of valuations unprecedented in a decade plus.

Other Factors Playing into Weak Stock Prices

Other factors have also been playing into weaker stock prices.

- The past several years of expansive monetary policy and fiscal largesse have greatly eased access to money, serving to pump up purchases of equities. Valuations have been driven way beyond historical norms which used to look to earnings per share. In fact, for many newly minted high-tech firms, billion-dollar-plus IPOs have been realized with no backup earnings whatsoever. A surface covering of unreality is being stripped away.

- Much of the froth in stock market activity during the pandemic has been due to inexperienced individuals, stuck at home and flush with cash (given they’ve had few outlets for spending), deciding to take a flyer on investing. Many of those neophytes, unfamiliar with the maxim of waiting out the bad times, are facing the ‘bear’ and bailing.

- Low interest rates and relaxed lending have made it easy, of late, to buy shares on ‘margin’. Now, the flip side is rearing up. Rates are climbing, share prices are descending and margin ‘calls’, initiated when the ratio of collateral to debt falls below a pre-set minimum, are exacerbating a trend towards equity selloffs

Among major stock market indices globally, Hong Kong’s Hang Seng index has experienced the biggest drop year over year, -26.6%. Two other indices with notably sharp declines y/y have been ‘iShares Emerging Markets, Asia’, -21.7%, and iShares (all) Emerging Markets, -20.0%.

On a cheerier note, at +8.2%, London’s FTSE in April achieved a y/y gain that was nearly equal to the TSE’s +8.7%. Also, the FTSE was the only index among the 14 showcased in Graph 6 to squeak out an advance month to month in April, +0.4%.

Stock markets, when they’re roaring, tend to boost what has been termed the economy’s ‘animal spirits’. An increasing wealth effect makes everyone holding assets in online or brokerage accounts, 401(k)s, mutual and pension funds feel upbeat.

When the opposite occurs, gloom has an opportunity to sneak in and cast shade on the prevailing mood.

Table 1

Graph 1

Graph 2

Graph 3

Graph 4

Graph 5

Table 2

Graph 6

Alex Carrick is Chief Economist for ɫ��ɫ. He has delivered presentations throughout North America on the U.S., Canadian and world construction outlooks. Mr. Carrick has been with the company since 1985. Links to his numerous articles are featured on Twitter , which has 50,000 followers.

Recent Comments

comments for this post are closed